Why choose a Ubank home loan

How we Lighten Your Loan

Which home loan is right for you?

Explore your loan options

We keep things simple. Ubank has a few home loan options to choose from, all with low fees and flexible features to help you get ahead.

Neat variable

Variable rates fromOwner occupiedP&Iup to 60% LVRMonthly repayments

$3,249.07

Estimated starting repayments based on a $500,000 principal and interest (P&I) loan over 25 years.

Flex variable

Variable rates fromOwner occupiedP&Iup to 60% LVRMonthly repayments

$3,249.07

Estimated starting repayments based on a $500,000 principal and interest (P&I) loan over 25 years.

Flex fixed

Owner occupiedP&Iup to 60% LVRMonthly repayments

$3,372.91

Estimated starting repayments based on a $500,000 principal and interest (P&I) loan over 25 years.

How to start your home loan journey

Let’s get you started

Get your free copy of Ubank’s Home Buyer Survival Guide

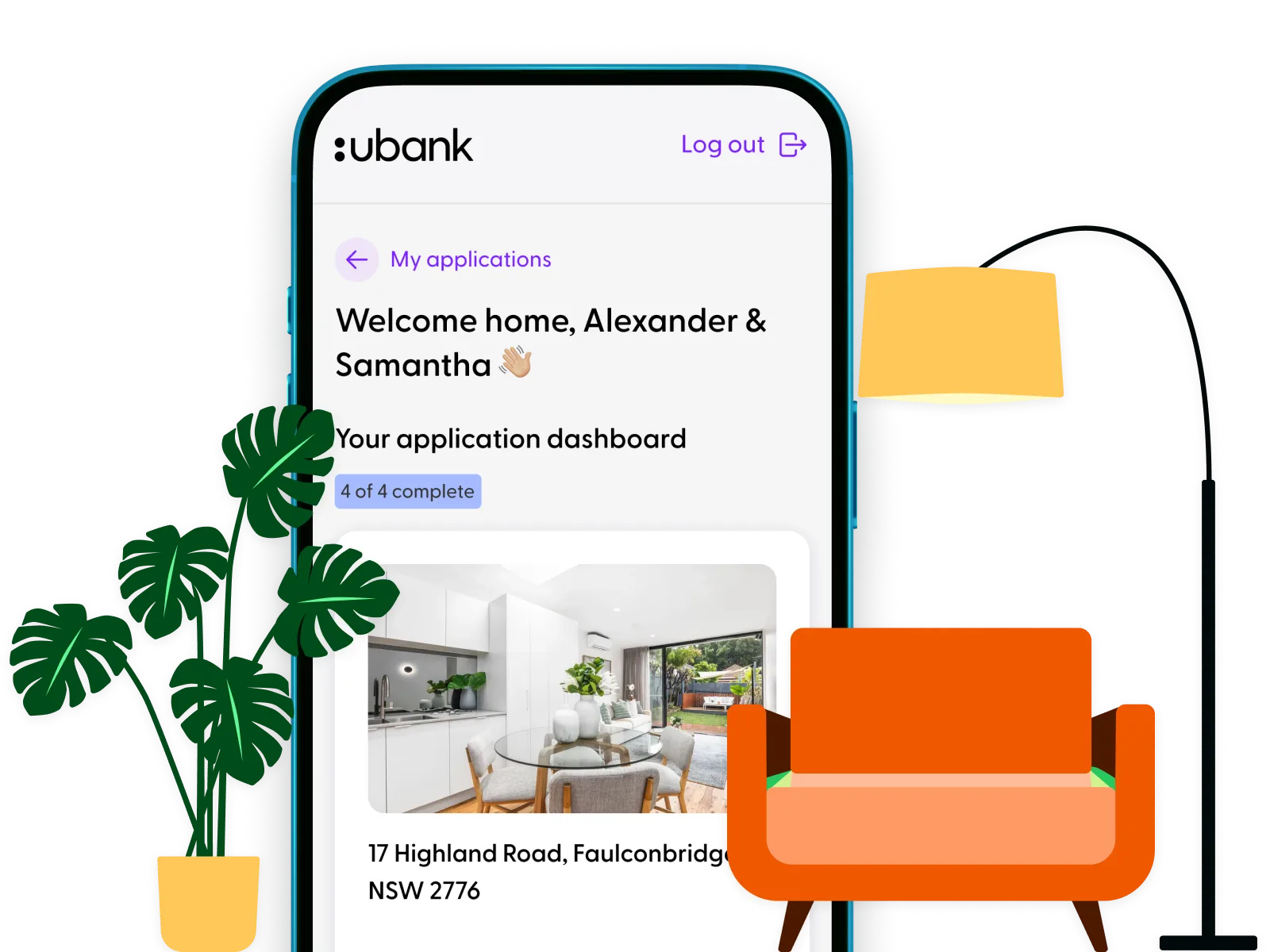

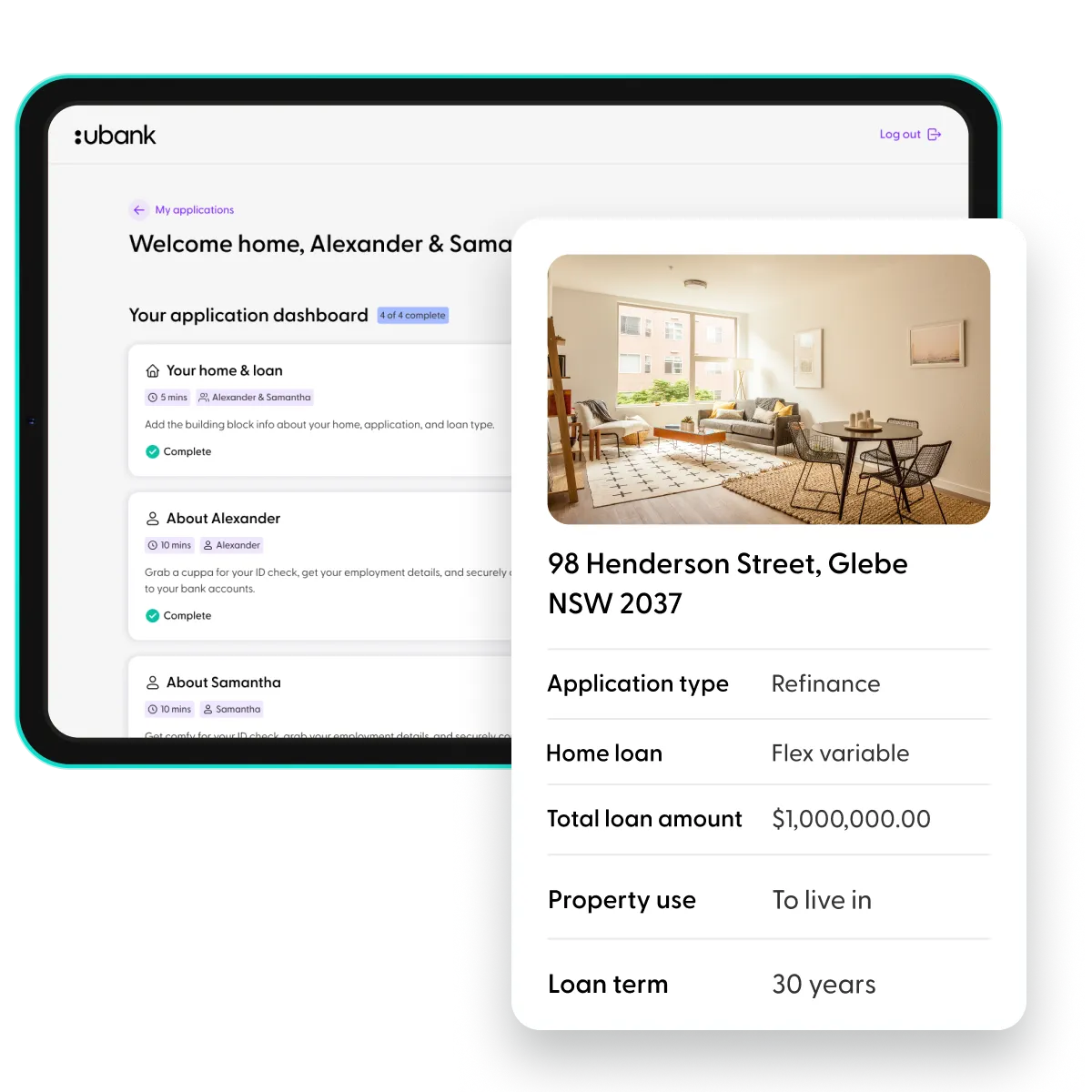

Get your loan done from home

Simple application

Complete our easy online application. If you need support, our lending specialists are ready to help at every step.

A fast result

We’ll review your application quickly and if everything’s good we’ll arrange a property valuation.

Seal the deal

Review your documents and accept your loan offer online, and we’ll guide you through to settlement.

Take a step closer to home

Apply now

Ready to take the leap with a Ubank home loan?

Articles about property

Become a property Pro

Buyer's agents, solicitors and conveyancers

6 Sep 2022

Here's why you may need an agent, conveyancer and solicitor when buying a new home.

Read more

Offset accounts made simple

8 Jan 2026

The more money you have in your linked offset accounts, the more interest you’ll offset.

Read more

What happens when you refinance?

31 Jan 2023

Is your current home loan not working for you? If you’ve discovered that you’re eligible for a lower interest rate, or perhaps you simply wish to change lenders, it’s useful to understand how a refinance application differs from an initial home loan application.

Read more

All the fine print